Watch Your Planner’s Planning!

Henry K. (Bud) Hebeler

6/9/10

I’m not a stranger to long-range planning after being responsible for Boeing’s long-range planning for six years and many presentations to a very savvy board that asked piercing questions—unlike what a financial planner is likely to hear from a trusting client. In today’s climate I would be asked questions about the influence of our massive debts—internationally, nationally, local and personal. I’d be asked how relevant historical return and inflation data were and what is likely to happen to tax rates. I’d respond with a dismal picture of the future with likely deepening recession followed by high inflation and amplified by the demographic changes to an ever increasing percentage of elderly.

Then the questioning would likely turn to national consumption as it affects the economy. Someone would undoubtedly ask if those retiring had enough money saved to retire as well as the effect of lack of savings on the future. After more than two decades of declining savings that began in 1985, I’d have to answer that that it would take more than 20% national savings rate for more than the next twenty years to catch up to the savings balances that pre-1985 savings rates would have produced. That doesn’t count for the fact that people should have been saving more considering that over those same past years, employers made a major shift to defined contribution plans that require even more savings. Such high savings rates just aren’t going to happen. That would require conditions even more severe than in World War II where supplies and goods were rationed, and many things were impossible to buy including cars and electronics. Further, such conditions would have to be tolerated for decades, not years.

Unlike the planning done in major industrial firms, financial planners typically buy or lease some software to make projections and compare a couple of alternatives for clients. Much of the common software is based on Monte Carlo simulations using indexes provided by others. Little is asked about the relevancy of either these data or the algorithms within the programs.

Some planning programs have elaborate tax calculations in spite of the fact that both tax rates and tax sources change almost every year, something that would not be lost on a board of directors. The unstoppable growth of entitlements will certainly take its toll. A value added tax will reduce consumption at the expense of the economy, but there’s not enough income to support entitlements with an income tax.

Almost all retirement projections are based on the assumption that the retiree’s expenses will increase with inflation and not exhaust retirement savings until some relatively safe period of time. Monte Carlo programs dress this up with a “success probability,” often expressed down to the closest 1%, and I’ve even seen closest to the nearest 0.1%. One well known financial planner said that he needed one-million simulations, not the typical 500 or 1,000, for each of his data points to get an “accurate” result. Of course there is no such thing as an accurate projection of the future. None of us know what the future will be. What is important is that we make wise decisions for budgets, Social Security, pensions, annuities, and defensive investments that will help us withstand some of the adverse things that can happen.

It’s for those reasons that I’ve learned to look at historical results differently than as a statistical representation of what might happen in the future. I think planning programs should be used to gain perspective and consider historical returns and inflation in the order they actually happened, not in the unrealistic fashion of Monte Carlo programs where returns are ordered randomly and inflation may be an overly simplified afterthought. The problem we now have is that the past statistics do not represent the cumulative results of decades of over-consumption, record debts at all levels and a huge shortage of savings. It’s hard to believe that the future is going to be as good as the past for a number of decades. I cringe when I see those panglossian Web programs with high default values for retirement returns.

But then again, I can’t see the future any better than anyone else. As a part of the remaining population that was brought up in the Great Depression, it really bothers me that everyone including the government wants people to spend, not save and make it easier to obtain debt. Common sense tells us that this is going to cost the nation plenty—we just don’t know when.

The use of inflation-adjusted spending in all of the models gave older people like many of my friends another kind of a problem. That’s because it encouraged them to spend too much too early. I’ll use a very simple example to show how both their financial planners and do-it-yourself software programs do this. The illustrations below come from the Free Retirement Planner on www.analyzenow.com.

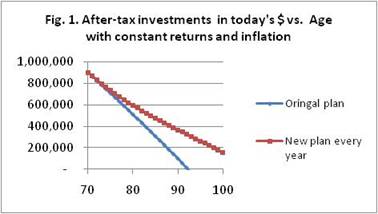

Figure 1 shows two

cases, each of which assumes constant returns and inflation: One is for an inflation-adjusted spending

analysis and the other represents what an older client might get from a

financial planner who makes a new plan for her client every year. The inflation-adjusted spending model runs

out of investments at some point leaving the retiree with just Social Security. The problem for the elderly retiree is that

she finds this out too late. Many years

ago, she and her adviser both considered that a portfolio that would last into

her nineties would be plenty of money.

But as she gets into her seventies, she starts to realize that she

better slow down on her spending or she’s not going to have enough money to

support her basic needs, much less the kind of lifestyle she enjoyed in her earlier

years.

Figure 1 shows two

cases, each of which assumes constant returns and inflation: One is for an inflation-adjusted spending

analysis and the other represents what an older client might get from a

financial planner who makes a new plan for her client every year. The inflation-adjusted spending model runs

out of investments at some point leaving the retiree with just Social Security. The problem for the elderly retiree is that

she finds this out too late. Many years

ago, she and her adviser both considered that a portfolio that would last into

her nineties would be plenty of money.

But as she gets into her seventies, she starts to realize that she

better slow down on her spending or she’s not going to have enough money to

support her basic needs, much less the kind of lifestyle she enjoyed in her earlier

years.

The other case in Figure 1 represents what would happen if the retiree did a new analysis every year—an approach I support. With an annual analysis, the investments are never exhausted, they just get smaller every year as the remaining investments get stretched even further. Those authors who think that older people just don’t want to spend more have been pouring over government statistics too long. They site that the elderly retirees could have spent more because they still have some investments left. Those statistics represent the fact that the majority of older people feel they have to get more conservative with their spending and worry whether they’ll have enough for assisted care or a nursing home that’s comfortable. The statistics say nothing about how much older people would spend if they felt they had the resources.

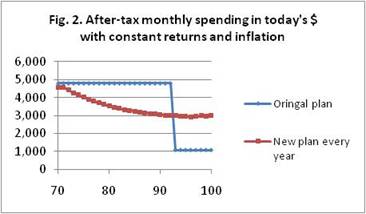

Figure 2 illustrates

the resultant spending for these two cases.

The inflation-adjusted spending fails after the investments are exhausted

just leaving Social Security or a pension or annuity. The other case for new planning each year

shows how drastically the spending must be reduced to preserve investments for

the future. This reduction is much more

severe for those who are more dependent on investments than Social Security or

other lifetime income. In real life,

this reduction can be very much larger due to security market failures,

unforeseen expenses, bad investment timing or choices, etc.

Figure 2 illustrates

the resultant spending for these two cases.

The inflation-adjusted spending fails after the investments are exhausted

just leaving Social Security or a pension or annuity. The other case for new planning each year

shows how drastically the spending must be reduced to preserve investments for

the future. This reduction is much more

severe for those who are more dependent on investments than Social Security or

other lifetime income. In real life,

this reduction can be very much larger due to security market failures,

unforeseen expenses, bad investment timing or choices, etc.

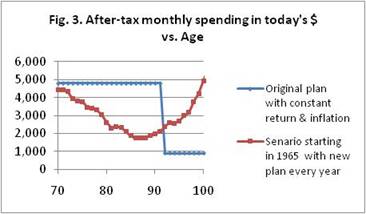

Real life isn’t like

the nice smooth lines shown on the previous figures. It’s bumpy for a number of reasons. One reason, of course, is that investment

values go up and down as does inflation. That effect is shown in Figure 3 with a

retirement scenario starting in 1965, the same unpleasant year to start

retirement as my father. If he had a

financial adviser, both would be very unhappy with the results as they unfolded

leaving planned spending values down over 60% in the example.

Real life isn’t like

the nice smooth lines shown on the previous figures. It’s bumpy for a number of reasons. One reason, of course, is that investment

values go up and down as does inflation. That effect is shown in Figure 3 with a

retirement scenario starting in 1965, the same unpleasant year to start

retirement as my father. If he had a

financial adviser, both would be very unhappy with the results as they unfolded

leaving planned spending values down over 60% in the example.

But there are other reasons real-life results have bumpy spending. There are surprise financial events that were unforeseen earlier such as problems with aged relatives or children or even grandchildren in desperate financial conditions. Almost every elderly friend I have had some significant adverse financial surprise that was beyond simple securities market failures. Of course another deviation from early plans is that elderly people usually gravitate to more conservative investments and/or chase the markets seeking higher yields or some quick recovery from stocks touted in the media that are already near their peaks.

I retired over twenty years ago, and most of our friends are also long into retirement. Many now recognize that they spent too much too early and have had to cut retirement budgets severely as well as downsize their homes. We have other friends in their eighties with enough resources so that they can still go on expensive trips, cruises, enjoy dining out, attend theater, hold private club memberships, buy luxury cars, give generous gifts to grandchildren, etc. As Sophie Tucker said, “I’ve been rich, and I’ve been poor. Believe me, Honey. Rich is better.” Or in terms our children may have to use, “I used to have sufficient money to pursue the things I wanted to do. Now I live in poverty. Poverty sucks!”

My plea is for people to give more recognition to the financial conditions of our times, be careful with assumptions used in commercial planning programs, assume very long lives, include some reserves for unknowns, use planning programs more for comparing results of alternatives than for “accurate” projections of the future, recognize that the future is unlikely to be like the past and ensure that investment management fees and costs are low because they are going to be an even larger drag on the smaller future returns!

Note: Illustrations are from the Free Retirement

Planner on www.analyzenow.com using 1.5%

financial costs and security indexes from Global Financial Data for $40%

S&P 500, 50% AAA corporate bonds and 10% short-term treasuries. Inflation history from

Bureau of Economic Analysis.